Key Takeaways

- Financial goals go beyond mere numbers; they're about what money lets you achieve, tied closely to your personal values.

- Make your goals real by making them measurable with specific amounts and clear deadlines.

- Categorize goals as short, medium, or long-term to help you prioritize and manage your money effectively.

- Regularly write down and review your goals to stay focused and adapt them as your life shifts.

What are financial goals, really?

Financial goals are not just abstract wishes for "more money." Instead, they are specific, measurable targets tied to real-life wants or needs, providing a clear purpose for your earnings and savings. We're talking about tangible outcomes, like getting that down payment for a house or paying off a specific student loan debt.

We often hear folks say, "I want to be rich." Or maybe, "I just need more cash." But those ideas are like trying to pack a suitcase for a trip without knowing where you're going. You'll probably end up with the wrong stuff, or maybe not enough, or way too much junk you don't need. A real financial goal is a destination. It's a house down payment, a child's college fund, or enough money put aside to start that small business you've been dreaming about. Each one is concrete. You can point to it. You can measure your progress toward it.

For instance, a real goal might be: "Save $30,000 for a down payment on a home by June 2028." Or, "Pay off my $25,000 in student loan debt by December 2026." Funding a child's education could be "Save $50,000 for my child's college tuition by their 18th birthday." See how specific those are? They aren't just vague hopes; they're measurable steps with deadlines.

The "why" behind these goals is just as important as the "what." Knowing why you want to buy that house—maybe it's to have a stable place for your growing family, or a yard for your dog, or simply to stop paying rent—gives you a strong emotional hook. That "why" is your fuel when things get hard, when you feel like skipping a savings deposit or splurging on something unnecessary. It reminds you of the bigger picture. We find that the more personal the "why," the more likely you are to stick with it. It's like training for a marathon: the finish line is the "what," but the personal best or the charity you're running for, that's your powerful "why."

Once we understand what a financial goal really is, we can start to see how different kinds of goals fit into our lives.

How can I identify my true financial desires?

To identify your true financial desires, we need to look inward, not just at numbers. Start by imagining scenarios where money solves specific problems or creates experiences. Think about what truly matters to you—security, freedom, or giving back. Distinguish between what you absolutely need and what you simply want.

It's easy to get caught up in what everyone else seems to be doing with their money, or what shiny things ads tell us we should want. But our real goals? They often hide just beneath the surface, waiting for us to actually sit down and listen. I find that a good way to start this self-reflection is with some specific daydreaming.

Imagining Your Life with "Enough"

I like to play a little game with myself. It goes like this: "If I had X amount of money, right now, what specific problems would it solve or what experiences would it create?" This isn't about wishing for a lottery win. It's about being concrete.

Maybe X is $10,000. Would that pay off your highest interest credit card, finally getting that monkey off your back? Or perhaps it would fund a small, quiet sabbatical to recharge? If X was $100,000, would it be a down payment on a small, cozy home, or maybe a nest egg that makes you feel genuinely secure for the first time? And if it were $1 million, would you travel the world, fund a local charity you care deeply about, or simply create enough passive income so you could work less and spend more time with family? Getting specific like this pulls those vague desires into focus. You start to see what truly makes a difference for you.

Needs vs. Wants: The Daily Juggle

Once you've done some of that imagining, we need to sort through those ideas like you're separating laundry—some things are absolute necessities, others are nice-to-haves. A need, financially speaking, is something that provides basic security, prevents hardship, or ensures essential well-being. This might be a robust emergency fund, enough to cover three to six months of living expenses if you lose your job. That's like putting a sturdy roof over your financial head.

A want, on the other hand, is something that enhances your life, brings joy, or fulfills a desire beyond basic survival. That exotic vacation you've dreamed of? Totally a want. The new car with all the bells and whistles? Often a want, even if you need a car. We can usually tell the difference if we ask ourselves: "Would my life fall apart without this right now?" If the answer is "no," it's probably a want. Both are fine, but knowing which is which helps us prioritize our money.

Aligning Goals with Your Core Values

The really deep stuff comes when we connect our money goals to our personal values—the things that truly matter to us in life. What makes you tick? Is it security, knowing you’re prepared for whatever comes your way? Or is it freedom, having choices and flexibility in your daily life? Maybe it’s contribution, wanting to give back to your community or support causes you believe in. For some, it’s experiences—collecting memories, not just possessions.

Think about moments when you've felt genuinely happy, proud, or fulfilled. What were you doing? Who were you with? What did that situation say about what you value? If you value family time, a goal to save for a family trip might resonate much more than saving for a fancy watch. If you value personal growth, maybe investing in further education or a coaching program becomes a key financial aspiration. When our financial goals sing in harmony with our values, it's not just saving money; it's building a life that feels authentic and rewarding. This deeper understanding will really help us as we look at how to sort these goals into different timeframes.

What's the best way to make financial goals measurable?

Making financial goals measurable means attaching specific numbers and firm deadlines to them. Instead of a vague "save more," aim for "save $10,000 for a down payment by December 2025." This clarity helps track progress, keeps you accountable, and transforms a dream into an actionable target you can actually hit.

We sometimes tell ourselves we want to "save more money," or "get out of debt." Sounds good, right? But it’s not really helpful. It’s like trying to hit a target you can’t see—a blank wall, maybe. You can throw darts all day, but you'll never know if you're hitting anything important. That’s what vague goals feel like. There’s no bullseye. No way to tell if you're even close.

Turning Vague Hopes into Clear Targets

So, how do we fix that? We get really, really specific. I mean, down to the dollar and the date.

Think about a goal like "start a business someday." That's a nice thought, but "someday" isn't on any calendar I know. Instead, we could make it: "Save $25,000 for a business startup by July 2027." See the difference? We now know the exact amount we need and exactly when we need it. This precision helps you build a real plan, step-by-step.

Here are a few more examples of how we can take a wish and make it something we can actually chase:

- Vague: "Pay off my credit card."

- Measurable: "Pay off $3,000 on my highest-interest credit card by June 30, 2025." (Now we know the amount, the specific card, and the deadline.)

- Vague: "Go on a nice vacation."

- Measurable: "Save $5,000 for a family trip to Disney World by Christmas 2026." (Specific destination, cost, and date.)

- Vague: "Build up an emergency fund."

- Measurable: "Have six months of living expenses—about $18,000 for my current budget—saved in a separate, easily accessible account by the end of 2025." (A clear amount and a solid timeframe, tied to a personal budget.)

We want to imagine what reaching that goal looks like, then write down the exact numbers and dates. It’s not just about dreaming; it's about drawing a map to get there.

This kind of clarity makes all the difference when it comes to figuring out how to actually achieve these things, and it naturally helps us sort out which goals we should tackle first.

How do I categorize and prioritize different financial goals?

To categorize and prioritize financial goals, we group them by timeline: short-term (under 1 year), mid-term (1-5 years), and long-term (5+ years). Prioritization is crucial because our money and time are limited resources. We decide which goals come first by weighing their urgency, impact, and feasibility, much like deciding which tasks to tackle immediately.

Once we know what we're saving for, and how much we need by when, the next step is figuring out where these goals fit into our lives. Not all goals are created equal, you know? Some feel urgent, others are more of a slow burn.

Sorting Our Goals by Timeframe

I like to think of our financial goals in three main buckets. It just makes things clearer.

Short-Term Goals (Under 1 Year)

These are things we want or need fairly quickly. They usually involve smaller amounts of money and have a pretty immediate impact.

- Emergency Starter Fund: This is like the first $1,000-$2,000 we try to stash away. It's for those annoying, unexpected expenses — a flat tire, a quick trip to the ER, or a leaky faucet. We really need this as a cushion.

- Small Debt Payoff: Maybe a credit card balance that’s just sitting there, not too huge, but it's nagging at you. Getting rid of these quickly can feel amazing.

- Specific Purchases: A new laptop, a weekend trip, maybe that fancy coffee maker you've been eyeing. Stuff that costs a few hundred or a couple thousand dollars.

These goals are often about building foundational security or enjoying smaller, immediate rewards. We usually aim to save up for these without taking on new debt.

Mid-Term Goals (1 to 5 Years)

These take a bit more planning and a bigger chunk of change. They're still visible on the horizon, but they aren't right here, right now.

- Solid Emergency Fund: Expanding that starter fund to cover three to six months of living expenses. For many, this could be $10,000 to $20,000 or more. This goal feels like a real safety net.

- Car Down Payment: Putting a good chunk of cash down on a car can save us a lot on monthly payments and interest.

- Larger Debt Reduction: Maybe taking a significant bite out of a student loan, or paying down a personal loan. These aren't overnight fixes but are totally doable in a few years.

- Home Down Payment (Initial Savings): Getting the first $10,000 or $20,000 together for a house might fit here, even if the full down payment is a long-term goal.

These goals often represent big steps toward a more comfortable, stable life. They need consistent effort over months or a few years.

Long-Term Goals (5+ Years)

Now we're talking about the big stuff. These goals require years, sometimes decades, of steady saving and often involve investing.

- Retirement Savings: This is probably the biggest one for most of us. Thinking about retirement means planning for a future many years away. It seems far off, but time really flies.

- College Savings: For kids, or even for ourselves if we're thinking about going back to school. Education costs a lot, and it definitely needs a long runway.

- Buying a Home (Full Down Payment): If we're aiming for a 20% down payment on a house, that's a serious amount of money and usually takes a long time to put together.

- Major Business Investment: Funding a big startup or expanding an existing business can mean saving up for many years.

These goals are about building lasting wealth and security far into the future. They feel less urgent day-to-day, but they’re incredibly important for our overall financial well-being.

Why Prioritize? Because We Can't Do Everything at Once

So, we have all these goals, right? And they all sound good. But here’s the rub: we usually don't have enough money or time to chase every single one at full speed. It's like trying to juggle a bunch of beanbags. Some of them are glass—those are the really important, fragile ones that will break if we drop them. Others are rubber—they can bounce around a bit, wait their turn, and not get ruined.

Prioritization is about deciding which goals are glass and which are rubber.

When I think about which goals to tackle first, I ask myself a few questions:

- What's most urgent? Does an immediate need trump a future desire? An emergency fund feels like a glass beanbag to me. Without it, any bump in the road can shatter everything else we're working on.

- What has the biggest impact? Sometimes paying off a high-interest credit card makes more sense than saving for a fun trip, because the interest is literally eating away at our money. Clearing that debt frees up cash flow and reduces stress.

- What's achievable right now? Starting small can be powerful. If a $20,000 down payment feels impossible, maybe aiming for the first $1,000 in a month is a better starting point. That builds momentum.

It's about weighing these things. We might put a smaller, short-term goal like building a starter emergency fund ahead of a mid-term car purchase, even if we really want that new car. Why? Because the emergency fund protects us from derailing all our other plans if something unexpected happens. We don't want to get into debt just because the car broke down.

This careful sorting and deciding lets us focus our energy and money where it matters most, ensuring we're always moving forward, even if it's just one step at a time. Figuring out this pecking order is actually easier once we have a clear picture of our spending and where our money goes each month.

Where should I write down and review my financial goals?

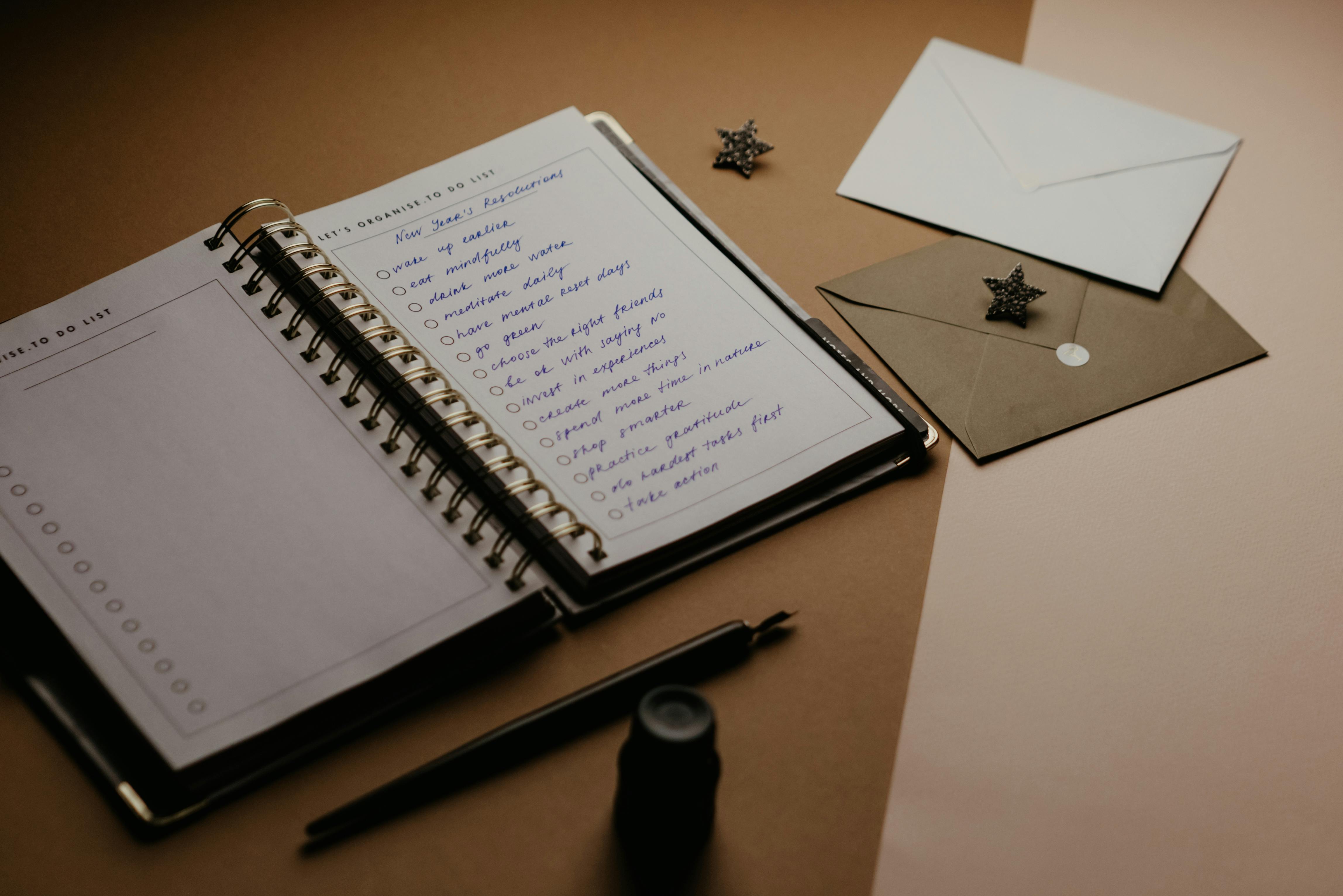

You can jot down your financial goals in a simple notebook, a digital spreadsheet, or a dedicated budgeting app. The key isn't the tool, but the act of making them tangible. Writing them down cements them in your mind and creates a record you can revisit. This commitment makes your aspirations feel more real and achievable.

I think about writing down goals like setting up a workbench. You don’t just think about building a birdhouse; you get out the plans, the wood, the nails, and you lay it all out. Our financial goals work similarly. They need a physical space, whether that's actual paper or pixels on a screen.

Simple Tools to Keep Your Goals in Sight

So, where exactly can you put these goals? It’s less about having the fanciest setup and more about having any setup that works for you.

- A Simple Notebook: This is old-school, but effective. There's something powerful about the physical act of writing things down. No distractions, just your thoughts and a pen. I've used a plain spiral notebook for years to just brain-dump ideas. You can easily dedicate a page to each goal and leave space to doodle notes or draw little progress charts.

- Digital Spreadsheets (like Google Sheets or Excel): These are fantastic if you like to see numbers move around. You can set up columns for your goal, target amount, start date, target date, and current progress. They're great for calculations and can automatically update percentages. You can even make charts to visualize your progress, which I find super motivating. It's like having a digital ledger where every penny has a purpose.

- Budgeting Apps (like YNAB or Mint): For folks who want more automation and integration, a budgeting app can be a real helper. Many let you set specific financial goals within the app, link to your bank accounts, and track your spending against those goals in real-time. They can take a bit of time to set up, but once they're running, they can offer a clear, instant picture of where you stand.

Regardless of the tool you pick, the actual writing down is the crucial bit. It moves your aspirations from fleeting thoughts to concrete plans.

The Power of Regular Review

Writing goals down is only half the job. The other half, the part that truly makes them useful, is reviewing them regularly. This isn't a "set it and forget it" kind of deal. We're talking monthly or, at the very least, quarterly check-ins. Think of it like a long road trip. You don't just put your destination into the GPS once and never look at it again. You check it for traffic, detours, and how far you've come.

Why is this regular review so important?

- Track Progress: You need to see if you're actually moving closer to your goals. Are you saving what you planned? Is your debt going down? Seeing the numbers change can be a huge motivator.

- Make Adjustments: Life happens. A sudden job loss, a new baby, an unexpected car repair—these things pop up. When they do, your financial goals might need a tweak. Maybe you need to pause saving for a vacation to rebuild your emergency fund, or perhaps a new work bonus means you can hit a goal faster.

- Redefine Goals: It's totally okay for goals to shift! Sometimes, what felt important a year ago doesn't quite fit anymore. Maybe you thought you wanted a big house, but now you're dreaming of early retirement. Reviewing allows you to prune old goals and plant new ones without feeling guilty. The process is about active engagement, not rigid adherence to a plan you made years ago. It’s okay to change your mind.

So, pick a time each month or quarter—maybe the first Saturday morning, or the day your paycheck hits—and sit down with your chosen tool. Look at your progress, adjust where needed, and celebrate the small wins. This active engagement keeps your money working for your life, not just some abstract idea of it.

Once your financial goals are neatly organized and regularly reviewed, the next big step is figuring out how to actually align your day-to-day spending with them.

Further Reading

After we talk about getting your goals organized and reviewed, you might want to learn even more. I know I did. These are some of the books and articles that really helped me think differently about my money and what I want it to do for me.

For Deeper Exploration

Read Next

View all articlesCross-Niche Validation: Find Your Unique Business Idea

Discover the power of the cross-niche method to uncover untapped markets and create unique business opportunities. Learn how to validate your ideas.

Early Retirement in Canada: FIRE vs. Government Benefits Age

Discover what age is considered early retirement in Canada. Explore FIRE movement goals vs. government pension ages (CPP, OAS) and public servant rules.

Debt Fatigue: How Financial Stress Sabotages Your Career Choices

Discover how debt fatigue silently steers your career, limiting opportunities and impacting well-being. Learn to break free from financial strain.

Etsy SEO Masterclass: Rank Handmade Goods on Page One

Unlock Etsy SEO secrets! Learn how attributes, long-tail tags, and shipping strategies get your handmade items to page one.