Master Your Money with YNAB: A Zero-Based Budgeting Guide

How to Better Budget with YNAB: Your Expert Guide to Zero-Based Financial Success

Introduction

For many, the idea of budgeting conjures images of restrictive spreadsheets, endless tracking, and the constant feeling of falling short. Traditional budgeting methods often lead to frustration, leaving individuals wondering where their money truly goes and why they can't seem to get ahead. This pervasive financial anxiety, however, has a powerful antidote in You Need A Budget (YNAB), a system designed to shift your perspective from financial constraint to empowerment.

YNAB offers a distinct approach, one that promises to simplify financial management and instill lasting control. It challenges the notion that budgeting must be complicated or time-consuming, suggesting that true money management can be distilled into "three habits and an hour a month" (YNAB Official Blog). This isn't merely about tracking past expenditures; it’s about proactively assigning every dollar a purpose, a strategy known as zero-based budgeting. Instead of merely reacting to where your money went, YNAB empowers you to decide where it will go. Think of it like this: your finances aren't a leaky bucket you're constantly trying to refill, but rather a team of specialized workers, and YNAB is the project manager, assigning each dollar a specific task before it even enters the system. This method paves the way for profound financial clarity, enabling users to gain command over their resources, plan for unexpected expenses, and confidently work towards their financial aspirations.

Understanding YNAB’s foundational principles and how they translate into daily practice is the first step toward transforming your financial life.

Key Takeaways

- YNAB implements a zero-based budgeting approach, ensuring every dollar is assigned a specific purpose for complete financial control.

- Successful YNAB usage centers on three core habits and requires approximately one hour per month, simplifying money management.

- Proactively address unpredictable expenses by consistently budgeting and setting aside fixed amounts within YNAB each month.

- Couples can effectively manage shared and individual finances using a three-budget strategy: one joint plan and two separate personal plans.

What is zero-based budgeting and how does YNAB utilize it?

Zero-based budgeting is a financial strategy where every dollar of income is assigned a specific job, such as an expense, saving, or debt repayment, until your income minus your expenses equals zero. You Need A Budget (YNAB) fully embraces this by requiring users to proactively categorize and allocate all incoming funds to specific budget categories before any spending occurs, ensuring every dollar has a purpose and preventing aimless expenditure.

At its core, zero-based budgeting operates on the principle of "giving every dollar a job." Imagine your finances not as a passive reservoir, but as a team of specialized employees. With zero-based budgeting, you, as the manager, assign each dollar a specific task—whether it's covering rent, saving for a vacation, or paying down debt—before it even begins its workday. The goal is to ensure that by the end of your budgeting period, typically a month, your total income minus your total allocated expenses and savings equals precisely zero. This doesn't mean you spend all your money; rather, every dollar is accounted for and intentionally directed.

YNAB, a "brilliant AI budgeting tool," leverages this technique to empower users with unprecedented financial control, as noted by an expert in a YouTube Tutorial & Honest Review. Instead of merely tracking where your money went after the fact, YNAB pushes you to make forward-looking decisions. When income arrives, whether it's a paycheck or a side hustle payment, YNAB prompts you to allocate those funds immediately into designated categories like "Groceries," "Utilities," "Emergency Fund," or "Fun Money." This proactive allocation is a fundamental shift from traditional budgeting, which often focuses on retrospectively categorizing past transactions or setting broad spending limits without a clear purpose for every single dollar.

How YNAB Implements Zero-Based Budgeting

YNAB's methodology is built around four core rules, with "Give Every Dollar a Job" being the first and most critical, directly embodying zero-based budgeting. This means:

Proactive Allocation

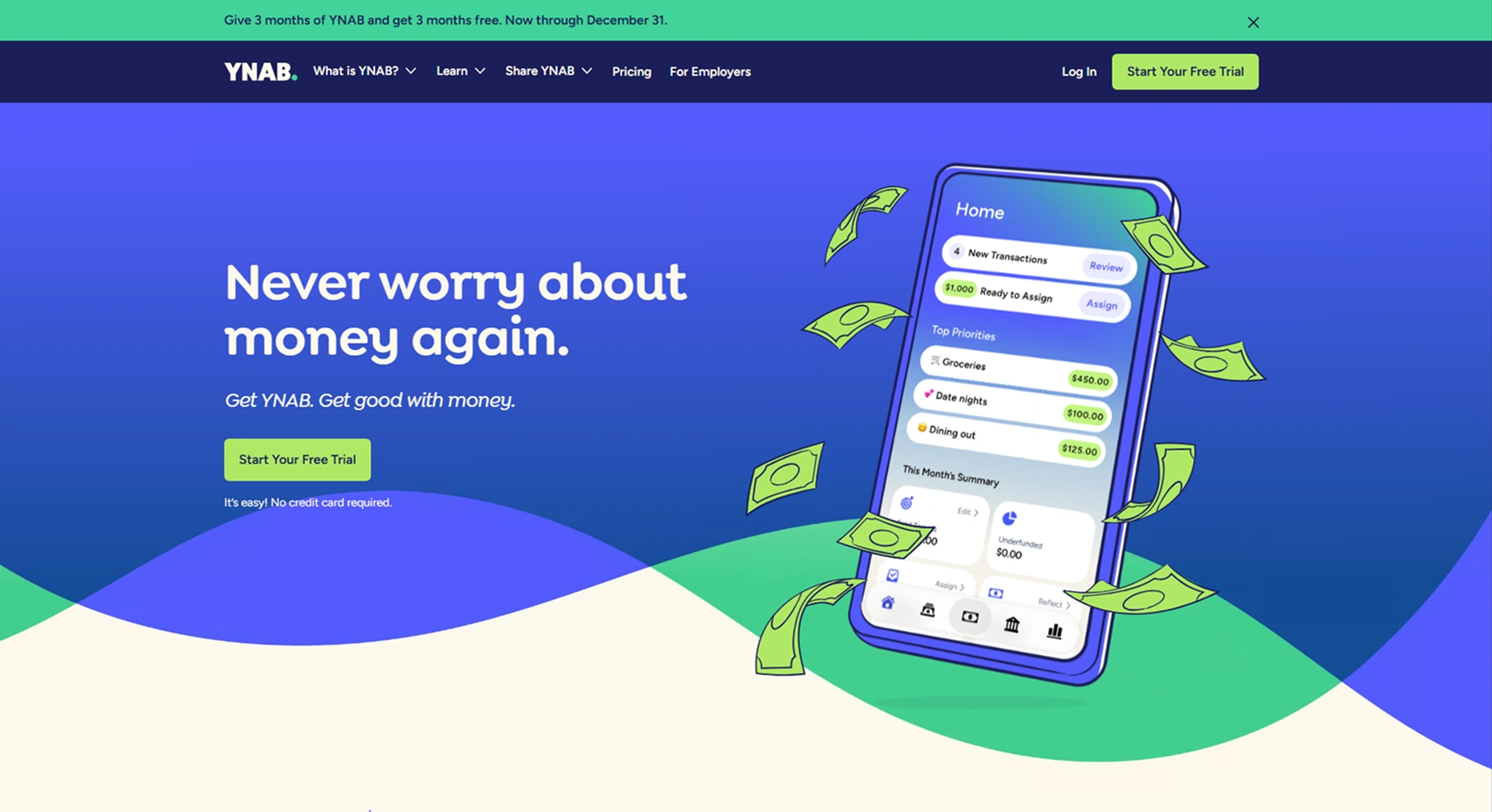

When money enters your YNAB account, it first sits in the "To Be Budgeted" category. Your immediate task is to assign every dollar from this pool to a specific category until "To Be Budgeted" reaches zero. This intentional act prevents money from being spent thoughtlessly. For example, if you receive a $2,000 paycheck, you might budget $800 for rent, $300 for groceries, $100 for transportation, and so on, until all $2,000 is assigned. The bottom line here is that YNAB transforms abstract financial goals into concrete dollar assignments.

Categorization and Goals

YNAB allows for highly detailed categorization, enabling users to create specific spending buckets for every conceivable expense, from recurring bills to infrequent splurges. Beyond just naming categories, you can set financial goals for them, such as saving $500 for a new car or budgeting $75 for dining out this month. These goals integrate directly with the zero-based allocation, making it clear how much you need to assign to each "job" to meet your objectives. This means you’re not just budgeting; you’re building a roadmap for your money.

Planning for Unpredictable Expenses

A common challenge in budgeting is unpredictable expenses, such as car repairs or annual insurance premiums. YNAB's zero-based approach encourages users to plan for these "true expenses" by setting aside a fixed amount each month. For instance, if car insurance costs $600 annually, you would budget $50 per month into a "Car Insurance" category. This way, when the bill arrives, the money is already there, having been given its "job" over several months. This strategy prevents financial surprises from derailing your budget, providing a crucial safety net.

In essence, YNAB doesn't just help you track expenses; it provides a framework to strategically direct your financial resources. This proactive system fosters a deep understanding of your financial inflows and outflows, creating a sense of control and purpose for every dollar you earn.

Moving forward, understanding the practical application of these principles in everyday YNAB use is crucial for transforming financial theory into actionable success.

What are the core habits YNAB recommends for effective money management?

Effective money management with You Need A Budget (YNAB) is built upon three core habits: giving every dollar a job, embracing your true expenses, and rolling with the punches. These principles empower users to maintain a clear, dynamic understanding of their finances, facilitating proactive decision-making and reducing financial stress. YNAB suggests that mastering these habits can streamline budgeting to approximately one hour per month (YNAB Official Blog).

You Need A Budget (YNAB) suggests that managing money with their tool "really only takes three habits and an hour a month" (YNAB Official Blog), transforming financial stress into clarity and control. These foundational practices are designed to integrate seamlessly into daily life, fostering a proactive approach to finances rather than a reactive one. They encourage users to engage consistently with their money, ensuring every dollar has a purpose and that the budget remains a flexible, living document.

Give Every Dollar A Job

This first habit is the cornerstone of YNAB's zero-based budgeting methodology, as discussed earlier. It means that upon receiving income, every single dollar is assigned a specific task or category, whether it's for bills, savings, debt repayment, or discretionary spending. The goal is to ensure your "To Be Budgeted" amount always reaches zero, preventing money from sitting idly or being spent without intent. This proactive allocation transforms your budget into a financial plan where you decide where your money goes before you spend it.

Actionable Advice: When your paycheck arrives, open YNAB immediately. Systematically go through each budget category, assigning funds until the "To Be Budgeted" amount hits zero. Start with your most critical obligations, like rent and utilities, then move to necessities like groceries, and finally to your savings goals and discretionary spending. The bottom line here is that assigning every dollar a role creates a clear financial roadmap and eliminates ambiguity about your funds.

Embrace Your True Expenses

Life is full of irregular, non-monthly expenses—car maintenance, annual insurance premiums, holiday gifts, or even just a new pair of shoes. The "Embrace Your True Expenses" habit encourages you to anticipate these costs and save for them gradually each month. Instead of being blindsided by a large bill, you forecast these expenses and break them down into smaller, manageable monthly contributions within your budget categories.

Actionable Advice: Identify all non-monthly expenses you anticipate in the next 12 months. For instance, if your car insurance is $600 annually, budget $50 each month into a dedicated "Car Insurance" category. If you expect a $300 car repair in six months, set aside $50 per month. This practice is much like understanding your car's maintenance schedule; you wouldn't wait for the engine light to come on for a routine oil change. Similarly, knowing your "true expenses" allows you to budget proactively, ensuring funds are ready when these costs arise, preventing financial emergencies, and making sure the money is there when you need it. As noted in the research, for unpredictable expenses like car repairs, YNAB users often suggest setting aside a fixed amount monthly.

Roll With The Punches

The third habit acknowledges that life is unpredictable, and budgets are not set in stone. "Roll With The Punches" means being flexible and adjusting your budget as circumstances change. If you overspend in one category, you don't abandon your budget; instead, you move money from another category with a surplus to cover the difference. This might mean reallocating funds from your "Dining Out" category to cover an unexpected medical bill or dipping into your "Entertainment" budget if groceries run a little higher than planned.

Actionable Advice: Regularly review your budget, ideally daily or at least several times a week, just as you would perform a quick check-up on your car's dashboard before a drive. If you notice a category running low or an unexpected expense arises, don't panic. Simply find another category from which to "steal" funds. For example, if you spent $20 more on groceries than budgeted, open YNAB, look for a category with available funds (like "Fun Money"), and move $20 from there to "Groceries." The bottom line is that this habit keeps your budget a realistic and functional tool, promoting adaptability rather than rigid adherence, which ultimately helps you stay on track despite life's curveballs.

These three habits, when consistently applied, create a powerful framework for financial clarity and control. By dedicating a small amount of time each day or week, users can proactively manage their money, transforming budgeting from a chore into an empowering process.

Understanding these core habits provides a solid foundation, but knowing how YNAB can adapt to different life situations, such as budgeting for couples, offers an even deeper insight into its versatility.

How can I effectively manage unpredictable expenses using YNAB?

YNAB helps manage unpredictable expenses by encouraging the creation of "True Expense" categories, where users proactively set aside a fixed amount each month. This builds a dedicated buffer for irregular costs like car repairs or medical bills. When unexpected expenses arise, YNAB's "rolling with the punches" philosophy allows flexible reallocation of funds, preventing budget derailment.

The Foundation: Embracing Your True Expenses

Effectively managing unpredictable expenses is a cornerstone of financial stability, and YNAB's approach is built around "Embracing Your True Expenses." This core habit involves acknowledging that many seemingly "unexpected" costs are actually predictable in their occurrence, even if their exact timing or amount isn't known. Think of these expenses like seasonal weather changes: you know winter will bring cold, even if you don't know the precise day the first snow will fall. Instead of being caught off guard, you prepare by buying a warm coat. Similarly, YNAB guides users to anticipate these larger, less frequent bills – such as annual car insurance premiums, holiday spending, or biannual dental check-ups – and allocate funds for them consistently throughout the year.

This method directly addresses the user suggestion identified in research: setting aside a fixed amount each month for these kinds of unpredictable expenses. For instance, rather than facing a large car repair bill and scrambling for funds, YNAB encourages budgeting for it incrementally. This transforms what might otherwise be a financial emergency into a manageable outflow of pre-allocated funds.

Creating Dedicated "True Expense" Categories

Implementing this strategy within YNAB involves establishing specific categories for these "True Expenses." This isn't just about saving money generally; it's about giving every dollar a specific job, even those earmarked for future uncertainties.

Setting Up Your Categories

To begin, identify common irregular expenses you face:

- Vehicle Maintenance & Repairs: Beyond gas, consider oil changes, tire rotations, and potential larger repairs like brake replacements or unexpected engine issues. Research highlights car repairs as a prime example of an unpredictable expense that users budget for proactively.

- Medical & Dental: Co-pays, deductibles, prescription costs, or even annual eye exams.

- Home Maintenance: Property taxes, appliance repairs, or routine upkeep like gutter cleaning.

- Annual Subscriptions & Memberships: Software licenses, gym memberships, or streaming services that bill annually.

- Holiday & Birthday Spending: These often come with predictable timing but variable amounts.

For each category, estimate the total annual cost. If your car insurance is $1,200 per year, divide that by 12 to get a monthly contribution of $100. If you anticipate $600 in holiday spending, you'd budget $50 per month. Even for truly unexpected events, like a sudden medical bill, you can create a general "Emergency Fund" or "Unexpected Expenses" category and contribute a fixed amount to it monthly, building a buffer.

Consistent Contributions and Building a Buffer

The power of this approach lies in consistency. Every time you get paid, a portion of your income is assigned to these "True Expense" categories, even if the expense isn't due for months. Over time, these categories accumulate funds, much like a well-tended garden accumulating produce. When the car repair bill arrives, or it's time for holiday shopping, the money is already there, ready and waiting. This proactive funding prevents debt accumulation and reduces financial stress. It’s akin to having a dedicated savings jar for each specific future need, ensuring that when the need arises, the jar is full.

For example, if you allocate $50 a month to your "Car Maintenance" category, after six months, you’ll have $300 available. If a $200 repair comes up, you simply assign the repair transaction to that category, and you still have $100 left for future needs. This provides clarity on your financial position and prevents sudden budget shocks.

Rolling With The Punches: Flexibility in Action

Even with diligent "True Expense" planning, life can still throw curveballs that exceed your budgeted amounts or introduce entirely new expenses. This is where the YNAB principle of "Rolling With The Punches" becomes critical. As discussed previously, this means maintaining flexibility and adjusting your budget as circumstances change, rather than abandoning it.

If an unexpected medical bill is higher than the funds you’ve accumulated in your "Medical Expenses" category, YNAB doesn't demand you go into debt. Instead, you "roll with the punches" by moving money from another category that has a surplus. Perhaps your "Dining Out" category has an extra $50 this month, or you decide to temporarily reduce your "Entertainment" budget to cover the medical cost. The important takeaway is that you retain control. You consciously decide which other category's funds will be reallocated to cover the overspending, ensuring your budget remains balanced and effective, even in the face of surprises. This adaptability is crucial for maintaining financial discipline without feeling overly constrained.

The bottom line for managing unpredictable expenses with YNAB is twofold: proactively save for known irregular costs using "True Expense" categories, and remain flexible with "rolling with the punches" when unforeseen circumstances demand a reallocation of funds. This combination ensures that your budget acts as a dynamic tool, empowering you to navigate financial challenges with confidence rather than succumbing to stress.

Next, we'll explore how YNAB’s principles can be effectively applied to the specific financial dynamics of couples, offering strategies for shared and individual spending plans.

How can couples budget together harmoniously using YNAB?

Couples can budget harmoniously with YNAB by adopting a "three separate spending plans" approach: one joint budget for shared household expenses and common goals, and two distinct individual budgets for personal discretionary spending. This method fosters transparency for collective finances while empowering each partner with autonomy over their personal funds, reducing potential conflict.

Successfully navigating finances as a couple requires more than just shared bank accounts; it demands a unified strategy that respects individual autonomy. YNAB offers a structured method for achieving this balance: creating one shared budget for joint expenses and two individual budgets for personal spending. This strategic separation, widely recommended by YNAB users and principles, provides a clear framework for financial collaboration while minimizing friction points often associated with combined finances.

The Three-Tiered Spending Strategy for Couples

Imagine your household finances as a cooperative gardening project. There's a main, shared garden plot that you both tend, where you grow essentials like vegetables and fruits that benefit everyone (joint expenses). Then, each of you has a smaller, personal plot where you can grow whatever exotic plants or flowers you desire without needing approval from your partner (individual discretionary spending). This is the essence of YNAB's three-tiered budgeting approach for couples:

- The Shared Budget: This central budget encompasses all joint financial responsibilities and common goals. Categories here might include rent or mortgage payments, utilities, groceries, shared transportation costs, insurance premiums, and saving for collective objectives like a down payment on a home, a joint vacation, or family emergencies. All income that is considered "joint" flows into this budget, and YNAB's "Giving Every Dollar a Job" principle ensures every dollar is assigned to a shared category. This provides complete transparency on where collective money is going, facilitating open discussion and agreement.

- Individual Spending Plans: Each partner maintains their own separate budget within YNAB, dedicated to personal discretionary spending. These budgets cover items like individual hobbies, personal care products, gifts for friends or family, clothing, dining out with personal friends, or any other expense that doesn't fall under shared responsibilities. By allocating a set amount of "fun money" or "personal allowance" to each individual's budget, YNAB empowers each partner to spend without needing permission or justifying every purchase to the other, a common source of conflict in traditional joint budgeting.

Fostering Transparency and Communication

The effectiveness of this three-tiered system hinges on robust communication and transparency. While individual budgets offer autonomy, the shared budget demands active participation from both partners. Regular budget meetings, perhaps a quick weekly check-in or a more comprehensive monthly review (as YNAB suggests only an hour a month is needed for effective money management, according to the YNAB Official Blog), become crucial. During these discussions, couples can:

- Review Shared Categories: Discuss overspending or underspending in joint categories and decide on adjustments together.

- Reconcile Goals: Reaffirm shared financial goals and ensure both partners are contributing equally, or agreeably, towards them.

- Adjust Allocations: Decide on how much money will be transferred from the shared income into each individual's discretionary budget. This can be a fixed amount, a percentage of income, or a proportion based on individual contributions.

YNAB’s interface naturally facilitates this transparency. Both partners can access the shared budget, seeing where every dollar is assigned and how much is available in each category. This shared visibility builds trust and encourages proactive problem-solving as a team.

Setting Shared Goals and Allocating Income

With YNAB, setting shared goals becomes a tangible exercise. For instance, if a couple aims to save for a $10,000 vacation in one year, they can create a "Vacation Fund" category in their shared budget and assign $833 each month to it. This explicit categorization, a cornerstone of YNAB's zero-based budgeting technique, transforms abstract aspirations into concrete financial actions.

Allocating income to both shared and individual budgets is another critical step. Many couples opt to pool all their income into one primary account and then "assign every dollar a job" within YNAB. From this pool, funds are first assigned to critical shared expenses and savings goals. Then, agreed-upon amounts are allocated to each partner's individual spending budget. This ensures that essential bills and common goals are prioritized before personal discretionary funds are distributed. This process aligns with YNAB's core philosophy of planning for every dollar before it's spent.

Managing Individual Discretionary Spending

The power of the individual spending plan lies in its ability to grant financial freedom within a responsible framework. Each partner can track their personal "wants" without impacting the joint budget or feeling accountable for every small purchase. This dedicated category functions as a personal "allowance" or "fun money" pot. For unpredictable individual expenses, like a sudden desire for a new gadget or a spontaneous outing, the individual can use their own budget without needing to "roll with the punches" from the joint household funds, unless they choose to. This separation dramatically reduces arguments over personal spending habits, as long as both partners adhere to their assigned individual budgets.

Addressing Challenges and Fostering Financial Alignment

Couples often face challenges such as differing spending habits, perceived unfairness in contributions, or a lack of clarity on financial boundaries. YNAB's structured approach directly addresses these:

- Differing Spending Habits: By having individual budgets, one partner's tendency to spend more on hobbies doesn't deplete funds needed for shared responsibilities or their partner's personal interests.

- Perceived Unfairness: The shared budget explicitly shows all contributions and expenses, allowing for open discussion if one partner feels the burden is uneven. Adjustments can then be made collaboratively.

- Lack of Clarity: YNAB forces clear categorization. Every dollar's job is visible, eliminating ambiguity about who is paying for what or why money is disappearing.

Ultimately, YNAB helps couples shift from a mindset of "my money" versus "your money" to "our money for our shared life" and "my money for my individual interests." This fosters financial alignment, turning potential conflicts into opportunities for collaboration and mutual understanding, transforming budgeting from a chore into a tool for strengthening the relationship.

Next, we will look at how beginners can overcome common hurdles when first starting with YNAB.

What are common pitfalls to avoid when starting with YNAB?

New YNAB users commonly struggle with over-categorizing, failing to fully trust the zero-based budgeting system, and getting discouraged by the initial learning curve. To navigate these challenges, begin with broad categories, actively practice the "rolling with the punches" philosophy, and utilize the robust support offered by YNAB's official resources and its user community.

Over-Categorization and Initial Complexity

One of the most frequent mistakes new YNAB users make is creating too many categories right from the start. Imagine trying to organize a new house by assigning a unique drawer to every single item before you've even moved in; it quickly becomes overwhelming. This "category creep" can lead to confusion, make budgeting feel like an impossible chore, and discourage users before they even begin to experience YNAB's benefits. Instead of clarifying finances, an overly detailed budget becomes a bureaucratic tangle.

Bottom Line: Start with a few broad, essential categories like "Groceries," "Rent," and "Transportation." You can always add more specific categories as you become more comfortable with the system and understand your spending patterns better. The goal is to gain control, not to achieve perfect granularity on day one.

The Expectation Gap: Trusting the System

Many new users give up too soon because they don't fully trust the YNAB system, particularly its core "zero-based budgeting technique." This method requires "giving every dollar a job," which can feel restrictive or counterintuitive if you're used to traditional budgeting. The expectation of instant financial clarity without active engagement can be a significant pitfall. When unexpected expenses arise, some might abandon the budget rather than adapt. However, the YNAB Official Blog emphasizes that managing money with their tool effectively only requires three habits and an hour per month, suggesting that consistency, not perfection, is key.

Bottom Line: Trust is built through practice. Commit to using YNAB consistently for at least a few months, even if it feels clunky initially. Recognize that the system is designed to be flexible and forgiving.

Overcoming the Learning Curve

Like learning any new skill, mastering YNAB comes with a learning curve. Financial management with a new tool is not a one-time fix; it's an ongoing process of skill development. Users might get discouraged when they misallocate funds, forget to categorize transactions, or face unexpected shortfalls.

Start Simple and Adapt

The initial setup and understanding of how YNAB works can be daunting. Resist the urge to replicate your old, often ineffective, budgeting habits within YNAB. Instead, embrace its unique approach. As mentioned, begin with simpler categories and gradually increase complexity as you gain confidence.

Embrace "Rolling With The Punches"

YNAB's "rolling with the punches" philosophy is crucial for long-term success, especially when dealing with unpredictable expenses. Life is full of financial surprises – a sudden car repair, an unexpected gift, or a forgotten bill. Instead of letting these derail your budget entirely, YNAB encourages you to adjust. If you overspend in one category, you simply move money from another less critical category to cover the shortfall. This adaptation prevents guilt and keeps you engaged with your budget rather than abandoning it. Think of your budget as a living document, not a rigid set of rules; it's meant to flex and change with your life.

Leveraging the YNAB Community and Resources

You don't have to navigate the learning curve alone. YNAB offers a wealth of resources designed to support new and experienced users alike:

- YNAB YouTube Channel: For visual learners, the YNAB YouTube Channel provides numerous tutorials and walkthroughs that break down complex features and budgeting concepts into easy-to-understand videos. Watching someone demonstrate the software can often clarify points that might be difficult to grasp from text alone.

- The r/ynab Community: The Reddit community, r/ynab, is an active forum where users share tips, ask questions, and offer encouragement. It's an invaluable peer-support network where you can find solutions to common problems, get advice on specific scenarios, and feel a sense of camaraderie with others on their budgeting journey.

- YNAB Official Blog: The YNAB Official Blog is another excellent resource for articles, guides, and strategic insights directly from the creators, helping users to refine their habits and understanding of the system.

Bottom Line: Don't hesitate to seek help and learn from others' experiences. The YNAB community and its official resources are designed to guide you through the initial hurdles and beyond, reinforcing that budgeting is a skill that improves with continuous learning and adaptation.

By actively avoiding these common pitfalls and leveraging the available support, new users can build a solid foundation for long-term financial success with YNAB.

Further Reading

For those looking to deepen their understanding of YNAB and further refine their budgeting skills, the following resources offer valuable insights and practical guidance:

Read Next

View all articlesCross-Niche Validation: Find Your Unique Business Idea

Discover the power of the cross-niche method to uncover untapped markets and create unique business opportunities. Learn how to validate your ideas.

Dividend Income in 2026: Real Portfolios & Living Off Dividends

Explore real investor portfolios in 2026 and the truth about living off dividend income. Learn key metrics, strategies, and practical steps to build your passive income stream.

Bundle Digital Products: Boost Sales & Order Value

Learn how to bundle digital products to increase average order value (AOV). Discover pricing, marketing, and selection strategies.

Financial Stability for Single Parents: 12 Practical Strategies

Discover 12 actionable ways single parents can build financial stability, from budgeting and debt reduction to income boosting and long-term planning.